封装回撤函数

在本节中,我们将创建一个回撤函数以在下一章中应用它。

在上面的内容里面我们已经创建的所有代码,为了方便调用,我们在这里将上面所有的功能包括Sortina系数、贝塔系数、阿尔法系数以及最大回撤等都封装在一个函数里面。

def BackTest(serie):

# Import the benchmark

sp500 = yf.download('^GSPC', proxy="http://127.0.0.1:10809")['Adj Close'].pct_change(1)

# Change the name

sp500.name = 'SP500'

# Concat the returns and the sp500

val = pd.concat((serie, sp500), axis=1).dropna()

# Compute the drawdown

drawdown = drawdown_function(serie) * 100

# Compute max drawdown

max_drawdown = - np.min(drawdown)

# Put a subplots

fig, (cum, dra) = plt.subplots(1,2, figsize=(24, 8))

# Put a Suptitle

fig.suptitle('Backtesting', size=20)

# Returns cumsum chart

cum.plot(serie.cumsum() * 100, color='#39B3C7')

# SP500 cumsum chart

cum.plot(val['SP500'].cumsum() * 100, color='#B85A0F')

# Put a legedn

cum.legend(['Portfolio', 'SP500'])

# Set individual title

cum.set_title('Cumulative Return', size=13)

cum.set_ylabel('Cumulative Return %', size=11)

# Put the drawdown

dra.fill_between(drawdown.index, 0, drawdown, color='#C73954', alpha=0.65)

# Set individual title

dra.set_title("Drawdown", size=13)

dra.set_ylabel('drawdown in %', size=11)

# Plot the graph

plt.show()

# Compute the sortino

sortino = np.sqrt(252) * serie.mean() / serie.loc[serie < 0].std()

# Compute the beta

beta = np.cov(val[['return', 'SP500']].values, rowvar=False)[0][1] / np.var(val['SP500'].values)

# Compute the alpha

alpha = 252 * serie.mean() - 252 * beta * serie.mean()

# Print the statistics

print(f"Sortino: {np.round(sortino, 3)}")

print(f"Beta: {np.round(beta, 3)}")

print(f"Alpha: {np.round(alpha * 100, 3)} %")

print(f"MaxDrawdown: {np.round(max_drawdown, 3)} %")

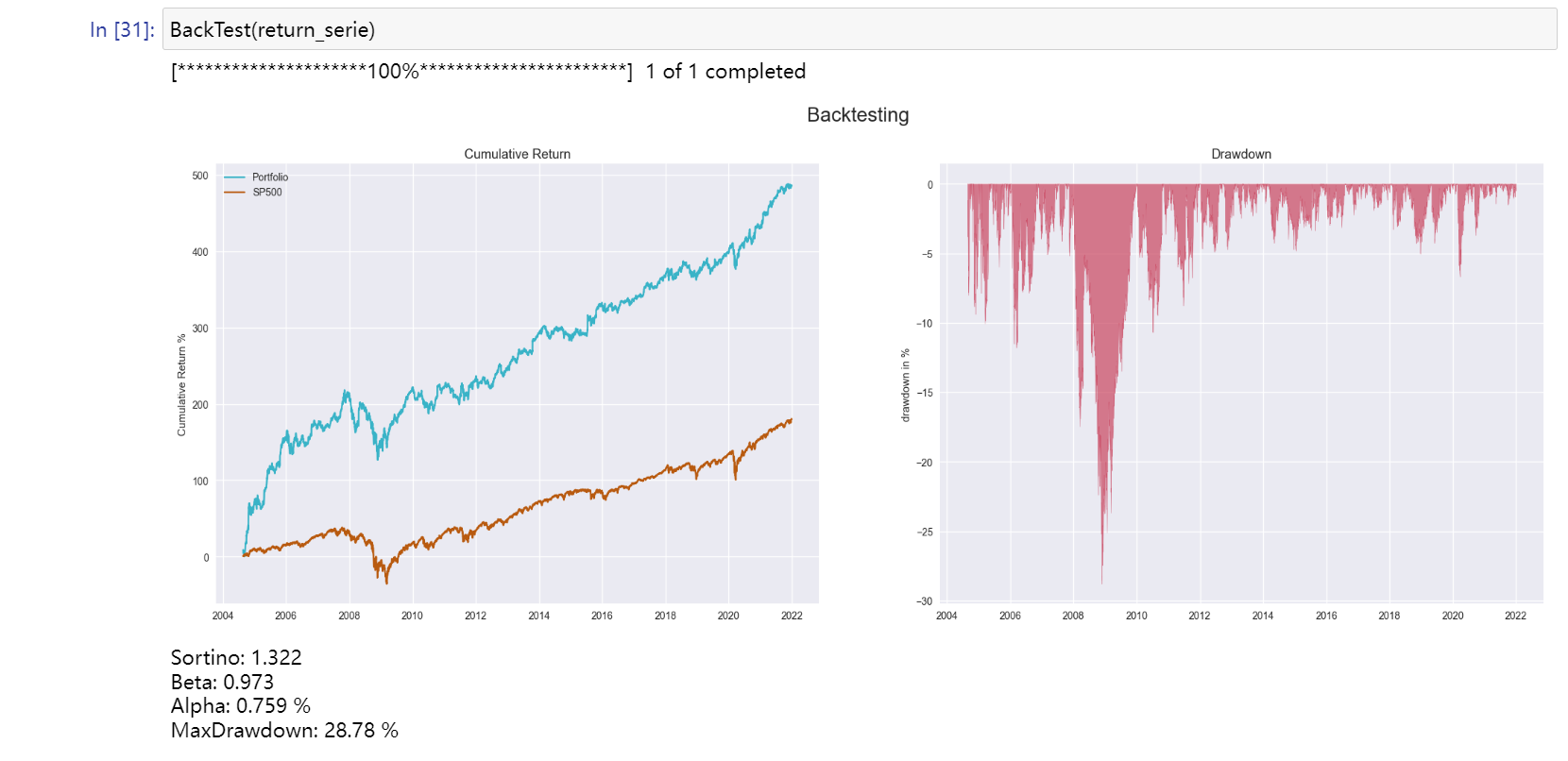

BackTest(return_serie)

原创文章,作者:朋远方,如若转载,请注明出处:https://caovan.com/10-shilianghuahuice/.html

微信扫一扫

微信扫一扫