封装实现计算过程的自动化

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

plt.style.use('seaborn')

import warnings

warnings.filterwarnings('ignore')

import yfinance as yf

import ta

def lin_reg_trading(symbol):

def feature_engineering(df):

""" Create new variables"""

# We copy the dataframe to avoid interferences in the data

df_copy = df.dropna().copy()

# Create the returns

df_copy['returns'] = df_copy['close'].pct_change(1)

# Create the SMAs

df_copy['SMA 15'] = df_copy[['close']].rolling(15).mean().shift(1)

df_copy['SMA 60'] = df_copy[['close']].rolling(60).mean().shift(1)

# Create the volatilities

df_copy['MSD 10'] = df_copy[['returns']].rolling(10).std().shift(1)

df_copy['MSD 30'] = df_copy[['returns']].rolling(30).std().shift(1)

# Create the rsi

RSI = ta.momentum.RSIIndicator(df_copy['close'], window=14, fillna=False)

df_copy['rsi'] = RSI.rsi()

return df_copy.dropna()

# Import the data

df = yf.download(symbol, proxy="http://127.0.0.1:7890")

# Take adjusted close

df = df[['Adj Close']]

# Rename the column

df.columns = ['close']

dfc = feature_engineering(df)

# Percentage train set

split = int(0.80 * len(dfc))

# Train set creation

X_train = dfc[['SMA 15', 'SMA 60', 'MSD 10', 'MSD 30', 'rsi']].iloc[:split]

Y_train = dfc[['returns']].iloc[:split]

# Test set creation

X_test = dfc[['SMA 15', 'SMA 60', 'MSD 10', 'MSD 30', 'rsi']].iloc[split:]

Y_test = dfc[['returns']].iloc[split:]

# Import the class

from sklearn.linear_model import LinearRegression

# Initialize the class

reg = LinearRegression()

# Fit the model

reg.fit(X_train, Y_train)

# Create predictions for the whole dataset

X =np.concatenate((X_train, X_test), axis=0)

dfc['prediction'] = reg.predict(X)

# Compute the position

dfc['position'] = np.sign(dfc['prediction'])

# Compute the returns

dfc['strategy'] = dfc['returns'] * dfc['position'].shift(1)

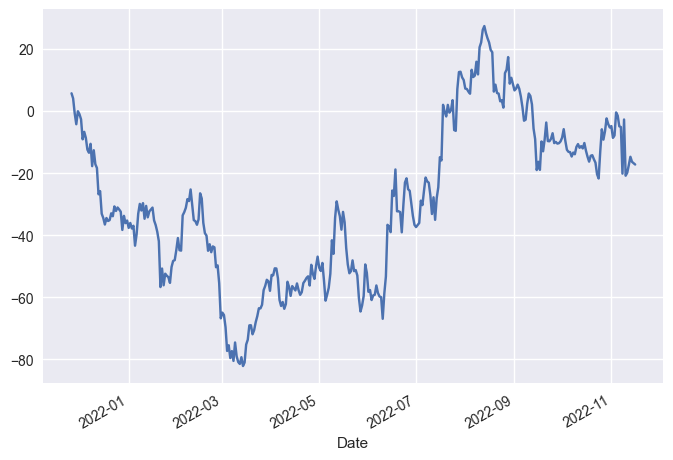

(dfc['strategy'].iloc[split:].cumsum() * 100).plot()

如果不需要科学上网,可以将

proxy="http://127.0.0.1:7890"内容删除;7890是clash的默认端口,如果你用的是其他科学上网的程序,请修改为你自己实际的端口;

调用该函数即可:

lin_reg_trading('ETH-USD')

原创文章,作者:朋远方,如若转载,请注明出处:https://caovan.com/09-xianxinghuiguisuanfazaijinrongdeyingyonganli/.html

微信扫一扫

微信扫一扫